Insurtech funding increased nearly 38% from Q4 2022 to Q1 2023, from about $1 billion to about $1.4 billion, according to a new analysis released by Gallagher Re.

The US leads France and the UK as the nation funding the most insurtechs. India and Germany round out the top five countries.

The definition of insurtech is important, according to Dr. Andrew Johnston, global head of insurtech and the author of Gallagher Re’s Q1 2023 Global InsurTech Report. Because the overall use of the term tends to be vague and overarching, the numbers captured will vary.

Currently 57% of global insurtechs — defined as technologically enabled, and those that offer technology as product and/or service to the insurance industry, such as software as a service (SaaS) — fit the “technologically enabled” business type. The remaining 43% of companies offering technology as a product or a service are “less likely to test the boundaries of …insurtech”.

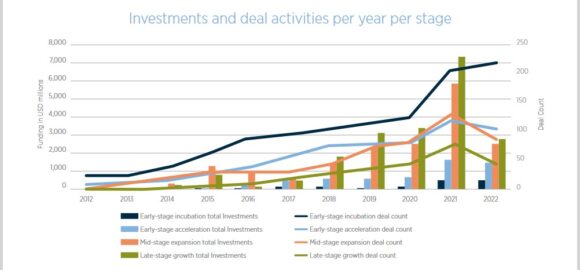

Within the insurtech funding cycle, four unique phases were identified: early-stage incubation, early-stage acceleration, mid-stage expansion and late-stage growth.

This initial report, a collaboration between Gallagher Re, Gallagher and CB Insights, focuses on Q1 and examines early-stage incubation funding, the funding activity captured during Angel, Convertible Note, Pre-seed, Seed and Seed venture capital (VC) deals.

The majority of insurtech investments from re/insurers occurred during the early stage for the sixth consecutive quarter.

Early-stage, also known as pre-seed, seed or angel investing, typically attracts investors who view themselves in a similar light. At this stage, investors are funding an idea and the founding members, since the product or service is unlikely to have been developed yet. Company valuations can fluctuate wildly at this stage and typical initial investors are the founders themselves.

The report found that 37.7% of all insurtech deals (as individual deal counts, not funding amount) were in the “early-stage incubation” category, a figure consistent with long-term insurtech data.

MassMutual Ventures led corporate venture activity among re/insurers in Q1 2023 with six investments. Five other re/insurers made multiple investments in Q1: Avanta Ventures (5), MS&AD Ventures (4), Munich Re Ventures (4), American Family Ventures (2), AXA Venture Partners (2) and State Farm Ventures (2) .

Notable partnerships identified in the report from Q1 2023 between re/insurers and insurtechs include: AXA XL and Document Crunch, Nationwide and Waffle, NEXT Insurance and LegalZoom, Progressive and Zendrive, Tokio Marine Kiln and LOADSURE.

Series C investments netted 20% of deals from re/insurers — the largest percentage since Q1 2019.

A source of much speculation was the unexpected dip in insurtech investing, after what appeared to be a steady rise over the course of several years. Careful examination led to a more realistic conclusion — 2021’s mega round of funding skewed the numbers. Rather than looking at 2022 as a significant loss, Gallagher Re suggests that 2022 figures are indicative of the overall course of isurtech funding over time.

In 2021, 62% of funding came from mega-rounds, while only 41% of 2022’s funding came from mega-rounds. In 2021, there were two noticeable periods of mega-round activity, according to the report; Q2 and Q4 (when combined totaled more investment than the entirety of 2022).

Going a step further, Gallagher Re removed the mega-round figures from 2021 overall insurtech funding and found it was a stable year, similar to the preceding years.

The detailed report states “while insurtech investment numbers look huge, a handful of standalone deals can, and do, have an enormous impact on the overall totals.”

Taking into consideration all deals from 2012 to present, 51% of all capital invested into insurtech came from mega-rounds. This, Johnston stated, suggests that a large amount of money invested in a handful of startups can greatly influence final numbers.

Additional analysis of both the mean and median averages provide a clearer picture. Early-stage funding reveals less deviation mainly because it is where the most volume is. Once funding moves to the mid and late stages, where check sizes rise, deviations in the average funding become more pronounced.

According to Johnston, “the key distinctions between funding rounds have to do with the valuation of the business, as well as its maturity level and growth prospects.” This impacts the type of investor involved and the reasons behind the need for capital.

Combining all deals together from 2012 to year-end 2022, across each investment life cycle, the report highlights the mean averages as follows; early-stage incubation $2 million, early-stage acceleration $12 million, mid-stage expansion $38 million and late-stage growth $110 million. Looking at all investment life cycles, the mean average insurtech investment round size is $22 million from 2012 to the end of 2022.

Though mega-round funding has been a significant funding source for insurtechs historically, the typically nine-figure fundraisers contributed to just 12.9% of total Q1 2023 insurtech funding, the lowest contribution rate since Q1 2020.

For many insurtechs, SVB was the go-to bank, the report’s author noted, indicating its demise could create more difficulty locating funding sources. Gallagher Re expects a significant reduction in the IPOs that might have been brought by insurtechs, unwilling to take on debt. In addition, strong M&A is expected.

Topics

Mergers & Acquisitions USA InsurTech Tech AJ Gallagher